In the second post of 2017 in our ongoing collaboration with New South Wales Young Lawyers’ International Law Committee, Marina Kofman examines the pros and cons of international investment arbitration.

In recent times, with growing citizen discontent about the effects of globalisation and rising inequality, many institutions and systems of global governance have come under fire. International arbitration is no exception. In particular, there has been public backlash in response to a proliferation of investor-State arbitrations. Investor-State arbitration involves the resolution by international arbitration of disputes between foreign investors, usually companies or natural persons, and the government of host States for the investment. The public concerns have been amplifying with the mega-regional trade deals currently being negotiated, most of which include arbitration as a dispute resolution mechanism.

Importantly, the criticism of international arbitration has not been as pronounced in the areas of international commercial arbitration, where the disputing parties are both commercial parties rather than a sovereign state, and less still against inter-State arbitration, in which two sovereign states submit a dispute to arbitration. This article will examine some rule of law issues that arise in the context of investment arbitration.

Features of investment arbitration

Investment arbitration is a relatively new form of arbitration. The first modern bilateral investment treaty, between Germany and Pakistan, was concluded in 1959. In the first thirty years of its existence, the International Centre for Settlement of Investment Disputes, which was established in 1965 and is the main arbitral institution administering such disputes, handled an average of only one case per year. Over the last ten years however, it has administered an average of forty cases per year. Its rapid growth over the last few decades is related to the proliferation of bilateral and multilateral and investment treaties and free trade agreements, of which there are more than three thousand known agreements today.

Criticisms against investment arbitration

Some criticisms expressed by the Australian public in their submissions to the recent Australian Senate enquiry into the Trans-Pacific Partnership, a far-reaching and comprehensive multilateral trade agreement, include rule of law concerns. These were broadly that:

- the resolution of disputes happens in “secret courts”;

- that the inclusion of ISDS mechanisms has a “regulatory chill” effect, which prevents the government from introducing public interest legislation, and diminishes our sovereignty;

- that the decision makers are powerful corporate lawyers and as such may make biased decisions, and are not accountable because they are ad-hoc decision makers rather than tenured judges, and

- that unlike with a court, there is no appeal available from the decision of the tribunal.

But are the sorts of criticisms, which together question the legitimacy of the entire system of resolving foreign investment disputes, justified? How too, does international arbitration compare to the other options for resolving foreign investment disputes?

Are the criticisms justified?

The public is justified in being concerned about these important rule of law issues in investment arbitration, which boil down to transparency; the continued power of government to regulate in the public interest; the independence and accountability of arbitrators; and the quality of decisions from which there is no appeal on the merits. Many of these valid rule of law concerns are addressed by mechanisms built into the arbitral process and the architecture of the investment arbitration system. Further, the arbitration community, including all the relevant stakeholders – users, arbitrators, states, and arbitration lawyers are constantly working to further refine the system to address known issues, such as those just mentioned.

a) Transparency

As investor-State disputes concern public interests, the process builds in significant transparency measures. For example, the vast majority of decisions are published online, just like court decisions, and the number of hearings open to the public and streamed online is on the rise. Further improvements are made on a continuing basis to address transparency concerns, including new international instruments such as the United Nations Commission on International Trade Law’s (‘UNCITRAL’) UNCITRAL Rules on Transparency in Treaty-based Investor-State Arbitration (‘Rules’), which may be adopted by parties to a dispute and the United Nations Convention on Transparency in Treaty-based Investor-State Arbitration 2014 (Mauritius Convention), which a state may adopt into its domestic law in order to give effect to the rules.

b) Loss of sovereignty and regulatory chill

An international treaty, concluded by two or more sovereign states, by definition involves both an exercise of state sovereignty in executing the agreement, and a self-imposed limitation of sovereignty which is manifest in the state’s agreement to abide by the treaty on its terms. The substantive protections in an investment treaty themselves guarantee to foreign investors certain rights that are consistent with a state exercising its powers in accordance with the rule of law.

For example, one common substantive protection granted by investment treaties is the protection against expropriation without compensation, which principle is enshrined in other international instruments such as the Universal Declaration of Human Rights and the European Convention on Human Rights. Similarly, the promise to afford an investor fair and equitable treatment imports notions of due process. There are a variety of such legal rights granted by relevant treaties that an investor must prove have a) been violated by a state’s conduct and b) have impacted the value of its investment in a host state before it is entitled to any compensation. Therefore, a mere complaint by an investor in relation to a government action will not suffice to create a meritorious claim.

Furthermore, states retain the power to regulate and take measures in the public interest as long as this is done in a manner consistent with the obligations in the treaty. Thus, the Australian Government’s Department of Foreign Affairs and Trade website notes:

“ISDS does not prevent the Government from changing its policies or regulating in the public interest. It does not freeze existing policy settings. It is not enough that an investor does not agree with a new policy or that a policy adversely affects its profits.”

In addition, available statistics in relation to this perceived ‘regulatory chill’, which is a particularly strong concern for the public, do not support the existence of a widespread chilling effect. For example, one study found that of all concluded ICSID cases up to 2014, 48% related to executive or administrative actions, whereas only 9%, related to legislative acts. Further, many such disputes about legislative measures were disputes by different investors relating to the same legislative measure, for example Jamaica’s decision to change tax rates for aluminum manufacturers is a legislative change that led to multiple disputes1.

c) arbitrator impartiality and accountability

In arbitration, the parties generally have an equal say in the constitution of the tribunal hearing their dispute. Typically, both parties will appoint an arbitrator each, and the two arbitrators will appoint the President of the tribunal. Arbitrators must make disclosures to the parties of any matters that call into question their independence and impartiality vis-à-vis the parties to the dispute, and parties have the right, frequently exercised, to challenge both the arbitrator’s appointment or the arbitral award on procedural grounds if they are dissatisfied. In addition, there are internationally accepted guidelines on conflict of interest, the IBA Guidelines on Conflict of Interest in International Arbitration prepared by the International Bar Association. UNCITRAL has also floated as a possible upcoming project the idea of developing an arbitrator code of conduct. Ultimately, it has been the absence of trust in the neutrality, integrity and competence of domestic courts and legal systems around the world that has given rise to a preference for arbitration.

d) no appeal on the merits and questions of consistency of decisions

The lack of available appeal on the merits in investment arbitration can raise valid concerns. However, this discounts the availability of limited procedural grounds for annulment of an award under the ICSID Convention or setting aside a non-ICSID award under the New York Convention on similarly limited due process grounds. The lack of an appeal on the merits of a decision is a long accepted feature of arbitration that encourages the finality of a decision and an end to a dispute. However the availability of due process grounds of challenge ensures the integrity of the arbitral process itself, and safeguards the rule of law.

Some have voiced criticism that investment arbitration awards are not consistent in their reasoning and decisions and that this makes the law unpredictable. As Immediate Past President of the International Bar Association, David Rivkin, pointed out in his 2012 Clayton Utz Address, substantive and procedural aspects of investment treaties and investment chapter drafting are largely similar. Tribunals interpret them and have eventually developed a body of law, which can be persuasive, but is not subject to a formal doctrine of precedent. This in turn contributes to the development of international law, for example by developing key concepts like fair and equitable treatment of foreign investors. That some parts of the law are as yet in a state of development and are unsettled is also a common features of domestic legal systems.

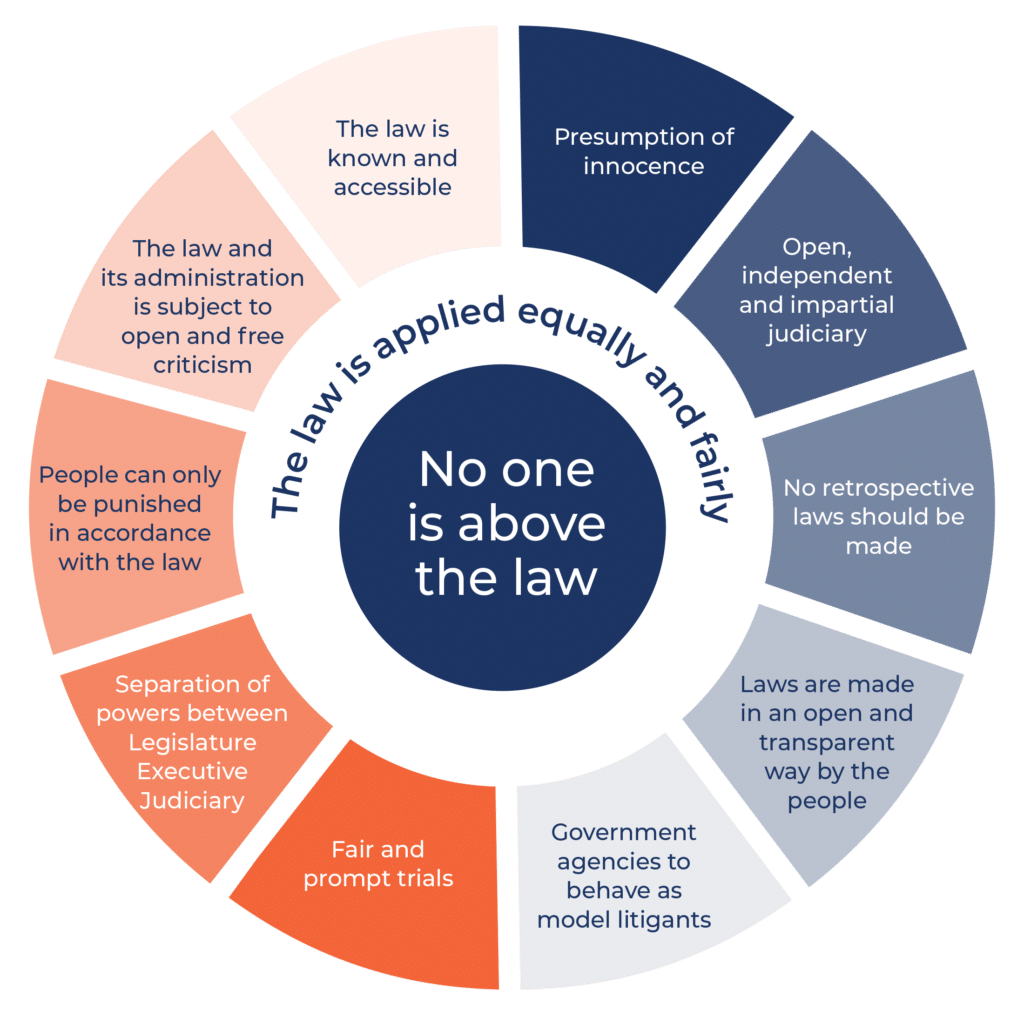

Features of Investment Arbitration and Lord Bingham’s Eight Principles

Another useful analytical tool would be to ask whether the system of international investment arbitration has indicia of the rule of law. An authoritative and oft-quoted list of features of the rule of law is the late Lord Bingham’s Eight Principles of the Rule of Law. These are:

- The law must be accessible and so far as possible, intelligible, clear & predictable;

- Questions of legal right and liability should ordinarily be resolved by application of the law and not the exercise of discretion;

- The laws of the land should apply equally to all, save to the extent that objective differences justify differentiation;

- Ministers and public officers at all levels must exercise the powers conferred on them in good faith, fairly, for the purpose for which the powers were conferred, without exceeding the limits of such powers and not unreasonably;

- The law must afford adequate protection of fundamental human rights;

- Means must be provided for resolving without prohibitive cost or inordinate delay, bona fide civil disputes which the parties themselves are unable to resolve;

- Adjudicative procedures provided by the state should be fair;

- The rule of law requires compliance by the state with its obligations in international law as in national law.

The features of the investment arbitration process that can be seen to align with Lord Bingham’s eight principles include the accessibility of clearly expressed international arbitration law and of reasoned decisions of tribunals; the defined rights and obligations contained in the substantive protections provided in the treaties themselves; access to a dispute resolution mechanism where an aggrieved investor can make a legal claim before a neutral and independent international tribunal and have it adjudicated according to law; and the growing body of international case law, which creates certainty and predictability of the law and reinforces a supranational rule of law standard for resolving foreign investment disputes. All of this in turn helps shape State behaviour towards adhering to rule of law norms when, in the exercise of their sovereign powers, they are impacting on a foreign investor’s rights under a treaty.

Comment

Despite the public outcry in the wake of claims against States, the available alternatives for resolving foreign investment disputes are less attractive from a rule of law perspective. First, there is the option of a diplomatic protection claim. This involves a government of an aggrieved investor petitioning the government of the host state on their behalf – an uncertain and unpredictable claim that is subject to political considerations. Second, in the absence of the investment arbitration option, aggrieved investors will typically be at the mercy of the domestic courts of the host State, which may be an unpalatable proposition considering the variance in the rule of law standards around the world. The availability of investment arbitration helps to promote the rule of law at an international level when domestic legal systems are inadequate.

It is not a perfect system and it is continuously evolving and being improved in accordance with user feedback. But it does uphold the rule of law by providing a neutral, apolitical forum for the resolution of international foreign investment disputes in accordance with international law and due process principles, and in circumstances where both the State and the investor have consented to the jurisdiction of the arbitral tribunal. Finally, the decisions of tribunals are enforceable, which ensures that justice is done, and helps to incentivise behaviour consistent with respect for the rule of law and international law.

Marina Kofman

NSWYL International Law Committee

Notes:

- Jeremy Caddel and Nathan M. Jensen, ‘Which host country government actors are most involved in disputes with foreign investors?’ (28 April 2014) Columbia FDI Perspectives No. 120, http://academiccommons.columbia.edu/download/fedora_content/download/ac:173530/CONTENT/No_120_-_Caddel_and_Jensen_-_FINAL_-_WEBSITE_version.pdf. ↩